“A journey of a thousand miles begins with a single step.” — Lao Tzu

Paraphrasing this maxim: to reach the right destination, you need a clear map. The same applies to business. Designing a fully digital mortgage process is not just a technical upgrade—it’s a strategic shift that touches every layer of the organization. It requires thoughtful planning, collaboration, and a deep understanding of customer needs. The payoff is real: improved operational efficiency and, most importantly, higher customer satisfaction.

Studies show that 53% of customers would prefer to sign a mortgage agreement without visiting a bank, and 46% prefer to submit documents electronically.

Table of Contents

Step One: Define the Vision

Understanding customer needs and expectations is essential. What is the primary expectation of a mortgage customer? To buy a property as quickly and effortlessly as possible. That’s why the process should be intuitive, transparent, and accessible online, allowing customers to manage various stages independently. Ideally, users should be able to navigate the process simply by clicking through clear, interactive elements on a website.

If they encounter any difficulties, support should be easily accessible.

When designing the mortgage process, we asked ourselves several key questions:

- How would we like to be served as customers?

- What tools are essential at each stage?

- Which areas can be improved?

Step Two: Choose Advisors and Tools

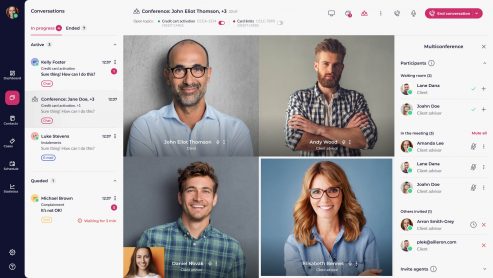

The role of the advisor remains vital, especially when dealing with complex financial products like mortgages. Due to legal requirements and product complexity, expert support is a key element of the process. Advisors offer knowledge, experience, and—most importantly—build trust, whether they’re based in a branch or operating as part of a remote service team.

Thanks to digital tools, advisors can now provide efficient support through video consultations and other remote channels.

An advisor should have access to functionalities such as:

- Video meetings with clients, including screen sharing and document presentations

- Online appointment scheduling for both clients and advisors

- Automated reminders before meetings

- Secure digital document exchange

- Electronic contract signing

This toolset enables a seamless advisory experience that mirrors an in-branch meeting—even when it’s fully remote.

Step Three: Digitize the Process

Digitalization dramatically shortens the time needed to complete a mortgage process. Leading banks invest in digital transformation not only for its efficiency, but also because of its direct impact on profitability. However, mortgages are still less likely to be sold remotely compared to other loan types—many of which are now predominantly managed via mobile apps or online banking.

Digital mortgage applications accelerate decision-making—cutting the traditional 30-day process almost in half—while also improving accessibility. Customers benefit most from the ability to complete formalities at a convenient time, without visiting a branch.

In banks that have undergone digital transformation:

- Average mortgage processing time was reduced from 30 days to 14–21 days

- 60–85% of clients preferred video consultations over in-person meetings

- 70–92% of applications were submitted online

- Customer satisfaction scores increased by 30%

Step Four: Prepare Teams and Optimize Continuously

Implementing a digital process also requires thoughtful team preparation. Training, consistent communication standards, and monitoring effectiveness are all essential to success. The saying “You only get one chance to make a first impression” captures the spirit of onboarding—transformation won’t succeed without internal advocates and early adopters.

Key preparation steps include:

- Training advisors in the use of new digital tools

- Establishing consistent customer communication standards

- Tracking key performance metrics and continuously optimizing the process

It’s important to remember that no process is ever truly “finished.” As customer expectations evolve and new technologies emerge, financial institutions must adapt continuously. Regulatory changes and shifting market demands also require ongoing adjustments to stay competitive.

Digitalizing mortgage processes – conclusion

Digitalizing mortgage processes is no longer optional—it’s a necessity in modern banking. Meeting customer expectations, investing in scalable technology, and maintaining a mindset of continuous improvement not only enhances operational efficiency, but also builds lasting relationships with clients.

Banks that embrace this transformation position themselves as industry leaders—redefining speed, service, and the mortgage experience itself.