Table of Contents

What Is Optichannel Approach in Banking?

Customers like to have a variety of options to choose from, but they will always have their favorites. This is true for products and their providers, but also for channels through which the customers can approach, or be approached, by their financial institution. The optichannel approach in banking means finding those favorites and utilizing them.

For instance, if a bank has an overwhelming amount of mobile-only customers, this particular channel is polished and personalized to let those clients use it as often as possible – without the need to, for instance, visit a branch for a consultation with an agent, or to verify their identity. On the other hand, this approach also means preserving physical branches in those areas where customers prefer traditional channels.

Why Is the Optichannel Approach in Banking Important?

According to the McKinsey Banking Consumer Survey [2], conducted in 2018, in countries like the UK, Netherlands, Spain, Germany, and France, over 50% of the consumers prefer digital channels over traditional ones for transactions, balance enquiries, and, in some countries, even for account opening. Yet, at the same time, less than 30% of the respondents claimed that they prefer digital channels for advice on complex products and less than 40% for help with technical problems. What does it mean in practice?

Customers have their preferred channels. This means that by utilizing them, thus adopting the optichannel approach, you will improve their overall banking experience and make them more loyal. As we know, this is especially important nowadays with the skyrocketing customer acquisition costs – you need to cater to those clients you have to avoid spending thousands of dollars on finding new ones.

Adopting Optichannel Solutions in Banking

Unlike adopting omnichannel support, opting for the optichannel one requires you to analyze your data. Who are your customers? What channels do they prefer? How many mobile-only clients do you have? You need to know the answers to these questions if you wish to tailor your services to the preferences of your customers.

For instance, if you’re focused on acquiring and maintaining younger, mobile-only customers, you have to make sure that physical contact via traditional channels is reduced to a minimum. This means implementing eKYC solutions that will let your potential customers set up an account quickly and easily via a mobile app and providing remote customer support, not only in the form of call centers and online chats but also via videocalls that your customers can schedule.

On the other hand, if you know that a particular region that you operate in is filled with customers who still opt for traditional banking, you need to make sure that there are enough physical branches in the area that your clients may go to.

Analyzing data is especially important in the second case. When optimizing your digital channels, you do it globally, but when doing so for the traditional channels, you do it locally, so you need to know where to distribute your resources (and where to pull them back).

Optichannel Solutions in Modern Banking

Combining the optichannel and omnichannel approaches is the key to success, one that you can obtain by utilizing the right banking solutions. Especially nowadays, when the number of clients using mobile-only and digital-only banking is high [2]. So, what should a good solution for embracing the optichannel approach in digital banking have?

- Videocall scheduling – Customers are discouraged by long waiting lines to reach a call center. Therefore, you need a system that lets them plan their meetings with advisors in advance.

- Digitalized procedures – If something can be done online, then it should be done online. The key to a fully optichannel experience is to reduce the need to switch from one channel to another to a minimum, which though easy in traditional banking – a client can always go to a branch – is a bit more difficult but possible in the digital realm.

- One solution – Clients don’t want to install different apps for different purposes, and your managers want to have one platform in which they can overview everything that is happening. This is why a good optichannel solution in banking should be a single platform/app that you can integrate your other systems into.

- Feedback – How to show your customers that you care? By asking for feedback. This will also help you improve your procedures further.

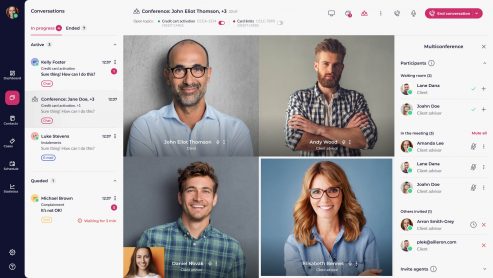

Our Livebank24 platform fits this description perfectly. It’s the true optichannel communication hub that will help you elevate your customers’ experience and attract new clients to your bank.

Optichannel Approach in Banking: Conclusions

The optichannel approach in banking lets you cater to the needs of your customers, thus improving their experience and building loyalty. With the costs of customer acquisition rising, switching to the optichannel approach is the best way to reduce churn and provide your clients with tailor-made services that they will find convenient to use.

You may also read: A roadmap for building a Customer Engagement Center

Sources:

[1]https://www.insiderintelligence.com/content/gen-z-mobile-banking-adoption-rise-banks-earn-trust