Table of Contents

How to add new value for digital customers?

To answer that question, let’s check a few facts:

1. When running a business, you should adapt the offer to customers’ expectations.

2. Customers’ shopping habits in digital environments are changing very quickly.

3. The number and value of remote purchase transactions are constantly increasing.

4. The banking sector has significantly supported digital evolution.

Customers are now ordering food deliveries, Netflix subscriptions, or shopping on Amazon from their couches. Customers now expect the same flexibility from banks. Every year, more product purchases are digital, such as a new bank account. But still, banks are selling many financial products in branches only. Such products include mortgage loans, consulting and investment products, advanced savings products, and individual insurance solutions. Traditional paths forced personal visits with a stack of documents, queueing, and wasting the customer’s time. However, changes are also taking place in these areas. Digital contract finalisation is becoming a standard affecting customer satisfaction and sales. Banks already need to think about how to model and maintain the loyalty of their customers while achieving their business goals. So, how to engage customers in banking? Banks need a Customer Engagement Centre.

Foundations of customer engagement in banking: understand consumer expectations

Customers prefer digital environments for many reasons, such as accessibility, speed, security, and convenience. The flip side is that customers like to feel special, or said another way, they like to get what they are looking for promptly. Therefore, digital spaces shape experiences using algorithms that propose content based on the customer’s previous choices. In the era of convenience, personalised experiences are not only the norm but also expected. With digital platforms, banks can provide an experience that feels familiar due to the customer’s use of other consumer platforms.

Banks must offer the value expected by the customer at every stage, whether mobile service, communication, or purchasing processes. It all comes down to using the right technology and listening to customer feedback.

Engage customers: communication is key

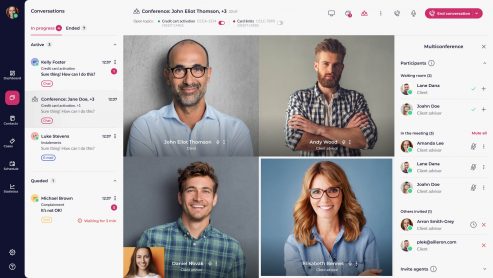

Communication is the stage in which we ensure that the advisor and clients have the same knowledge. The variety of communication channels means that customers may communicate via chat, e-mail, video, or telephone. Each channel allows the customer to engage in the process and provide relevant information. By adopting mechanisms that aggregate crucial communication channels, we enable the advisor to free themselves from extra work so they can focus on delivering the best experience.

The bank advisor clarifies the client’s needs and situation so they may best serve them. Only some customers feel comfortable with financial products, especially the more advanced ones. Even customers who use electronic banking daily will visit branches when buying an apartment or setting up an individual investment plan. Why? – because clients need to feel that the advisor is doing the best possible job for them.

Finding the communication sweet spot takes time. The advisor must be proactive. To assist them with this, advisors need a solution that includes customer journey tracking.

Keeping your messages organised on time will make your customers feel valued. Advisors, on the other hand, will save time and manage their work to be more effective. It’s a win-win situation.

Concentrate on what matters: managing customer journey pain points

Every customer who wants to buy a product has a different perspective, needs and expectations. They range from people coming to the process for the first time, without knowledge or expectations, to veterans with much experience. Recognizing this allows us to adapt the frequency of communications to each customer’s needs. Well-conducted communication facilitates the entire process for both the client and the advisor. Due to the availability of multiple channels, we can use each to its advantage when presenting an offer. Let’s take an example where customer John wants to buy an apartment. He experiences the stress of finding a suitable property and the credit process itself. He may feel lost in obtaining documentation; he needs to figure out what to ask and what next steps to take as he makes this purchase for the first time. The advisor should use his knowledge to educate the client. The more John knows what awaits him, the less stress he has and fewer doubts. He can move confidently through the next steps of the process.

As a Bank, you want customers to feel comfortable and to meet expectations while they use the service and purchase products. One of the best ways to achieve customer engagement in banking is maximum simplification and shortening buying paths.

How to Improve Customer Engagment in Banking? The advantages a Customer Engagement Center provides

Customer Engagement Center solutions recognise various pain points. They focus on building a tailored experience regardless of the many paths available for each customer outcome. This approach contrasts with mass products, where the same offers and scripts appear in every conversation. Understanding what customers want and how they want to receive information involves per-person preferences. Combined with the greater convenience of a fully-tailored experience, customers are more likely to feel comfortable, and they are less likely to consider looking for an offer from another supplier.

Let’s look at the features that help accelerate digital engagement.

1. Meeting manager

Nothing spoils an experience more than waiting in line, whether physical or digital. However, booking an appointment in an advisor’s shared calendar or sending a meeting proposal to the client makes it much more manageable.

First, the advisor has control over their calendar. Secondly, it reduces the risk of a customer resigning while waiting for a call. This is especially true for advanced product conversations, which can last an hour or more.

2. Digital document management

In many processes, delays in document processing can create bottlenecks. The exact causes of the blocks are numerous, such as the need to collect and deliver documents, manual processing, uploading to other systems, human error and other unforeseen events.

Using document repositories to which both the client and the advisor have access allows you to solve many problems. First, there are time savings from not delivering and transferring paper versions to the bank’s systems. Thanks to the ability to comment and notify documents, both parties to the process know what is happening to them.

Document automation constantly evolves, allowing you to reduce and optimise monotonous manual tasks. They shall also ensure that the relevant documentation is submitted and that all data fields meet the requirements and, if not, indicate the necessity and scope of the correction.

Additionally, reducing the need to handle and archive paper documentation reduces environmental impacts.

3. Visualisation and process stages.

We all know there are numerous steps in a digital purchasing process, but how can you make it easier for customers? Consider breaking down your digital process into smaller, more manageable steps to get started. Show what actions are needed and who is responsible for each step. In a mortgage, the steps are, for example:

a) Checking initial creditworthiness

b) Collecting the necessary documentation

c) Submitting a complete loan application

d) Analysis of the application

e) Contract proposal ready to sign

f) Loan payment.

This way, borrowers can see their path more clearly, and you can help them as they walk it. Of course, each stage contains subtasks to complete. Illustrating any challenges ahead of this can save the customer time.

By preparing your customers, you build their trust in you while reducing their anxiety. It also streamlines the process and minimises the risk of misunderstandings, making the paths much more transparent. You can even say if a task will be completed by hand.

4. Activate advisors

Today’s digital platforms must allow the client and the advisor to initiate contact, actively work with the application, or edit it at any time. In reality, clients face different circumstances and follow different paths. Therefore, we generally accept that customers belong to either a digital or hybrid category.

Whatever the case, you must provide a versatile platform to aggregate these customer habits and respond pragmatically. For example, sometimes the client gets stuck at a particular step or would like to find out the state of progress of their application. In both cases, the advisor reviews the case’s status, can verify their location, provide answers, or ask the client if they need help completing the application. This is what a flexible platform for assigning and monitoring tasks does, thus saving time and energy and reducing frustration.

Summary

When offers are comparable in a few clicks, user experience and recommendations provide an advantage over the competition. Providing customers with solutions that are easy to use and, at the same time, valuable is possible. Actions when implementing digital banking customer engagement must be thoughtful based on available resources and the ability to reliably map the customer journey. Even a state-of-the-art solution will only build customer loyalty if processes conclude with the required follow-up. Many banking processes still require the collection of a stack of documents and certificates. It takes a lot of the customer’s and bank’s time. In these situations, customer engagement decreases, and the risk of an abandoned process increases. The ability to reassure customers’ doubts is a great advantage.

Loyalty builds from previous conversations and experiences. Banks meeting the customer’s expectations at every stage, whether in mobile services, communication, or purchasing processes, achieve more valuable outcomes. The customer feels heard and understood by you. The quality of service for advanced products is as essential as the offer parameters.

Whether using the Customer Engagement Center solution for mortgages, or other processes, make sure you have a partner to help you map tasks and stages. With proper support, you can be sure you will develop an experience that meets your customers’ expectations and grows their trust.