Table of Contents

Omnichannel expectations

Banking customers now expect an integrated experience that includes multiple communication channels. Ideally, this should allow the customer to complete queries and transactions entirely within digital channels. However, the reality is that with complex issues and products switching between chat channels, video, and phone calls without interruption is rare.

Customers usually have to re-confirm their identity and repeatedly relay the same case details.

The utopian multichannel (or omnichannel) future that we’ve been sold in recent years remains in the future.

The question banking people ask themselves is: Will the omnichannel banking approach deliver on its promise anytime soon?

This article examines that question and, in seeking an answer, comes to a new understanding of optichannel that might be a welcome surprise for you.

Who should read this article? If you are facing a decision related to transforming your customer/client communications approach, this article intends to guide you with that. We also recommend it if you are involved in the digitalisation of banking customer care and want to keep up with the latest developments.

So, what is an omnichannel? Meaning

The term omnichannel first appeared in retail marketing in the early 2010s. Omnichannel marketing unifies sales and marketing into a single integrated customer experience delivered across all channels used by a brand, whether digital or analogue.

The story of omnichannel banking began with the vision that the same set of services could be made available to a bank’s customers across all channels. Whatever the digital venue, clients could perform the same banking operation, whether they used a website, a mobile app, spoke to a representative at a call centre or visited a branch. Soon after, real-time data synchronization allowed a customer support session to begin in one channel and finish in another without the need to interrupt the interaction and provide the same data over again.

Omnichannel became even more visible with the arrival of ‘virtual’ banks – branchless online banks where the entire customer journey is digital. And right now, COVID-19 lockdown measures have forced bricks-and-mortar branches also to reshape their service models, enabling remote communication with customers. Online banking customers are usually well-prepared for the digital-only banking experience, and they are primed to reap the benefits of simplicity, convenience and a sense of control.

Is omnichannel transformation needed?

The transformation to a deeper digital experience can be more of a challenge for traditional banks that are at an earlier stage of digitalisation. They will still have a significant segment of customers who prefer traditional channels such as telebanking or in-branch banking. However, even this segment, driven by new technology, including smartphones and voice-controlled virtual assistants, and the COVID-19 circumstances mentioned above, are becoming more comfortable with a digital experience in their lives generally.

The reasons for conventional banks to develop a complete digital offering now outweigh the costs of not doing it. A bank going down this route gains a wealth of data analysis possibilities to help them understand their customers’ needs in every part of the lifecycle. By applying data insights, the bank can deliver greater personalization, a more valuable offer and reduced customers churn. This leads to improved lifetime value from each customer relationship and greater profitability. The next ten years should be at least as dynamic as banks leave legacy systems behind and adapt to a focus on the individual customer rather than their product range and services.

Omnichannel evolution

Let’s take a moment to look at omnichannel banking’s main evolutionary steps.

The beginning of omnichannel

The initial advantage of omnichannel was that customers could use whatever channel they preferred to interact with their bank. They loved the fact that if they didn’t want to pick up a phone, they could send an email, initiate a chat, or even interact through social media. It was an entirely new world.

Empowering as it was for the consumer, it became cumbersome and costly for the companies supporting them. Communication streams and the related technology multiplied, making it harder to manage systems and staff cost-effectively. Agents had to toggle between systems and switch between queues. It wasn’t easy (or sometimes even possible) for an agent to know about other types of customer interactions.

The set of multiple – but essentially disconnected – channels meant customers could not switch from email to chat to a video call without repeating steps for providing identity verification and case information.

Moving on, the next evolutionary step sought to address some of these difficulties for banks while the experience adopted more interaction types that felt natural to the customer.

Omnichannel now

We now see channels connected via a single centralised routing system. The customer experiences seamless transition between channels and conversations and can use channels in combination, benefitting from what each is best suited to. Managers and customer service agents can log all interaction types and have global access to customer history, making the customer journey more coherent and accessible while still allowing it to be dynamic and non-linear.

What’s next, given that channels are already seamlessly integrated, and agents can transfer sessions between channels while maintaining continuity?

Future of omnichannel

The next step in omnichannel banking’s evolution will enable:

- Banks to have a deeper understanding of the customer and their needs by retaining their communication habits and preferences at a person-specific level. No two customers are alike, and each seeks help differently, too.

- In effect, each customer will have their own individual banking support channel, where no detail is ever forgotten or lost. Additionally, the bank can proactively offer support according to a highly detailed picture of each customer. This brings about a real revolution in seamless, continuous relations between the bank, its agents and each individual customer.

Multi-channel vs omni-channel

Multichannel and omni-channel: how do they differ?

Multichannel

- Allowing customers to transact with the bank via multiple channels

- Understand what customers need through analytics

- Based on a system of customer records

- Relying on SOA: integration of applications and messaging

Omnichannel

- Allowing clients to interact with the bank via multiple channels

- Try to understand what customer wants and likes through analytics

- Based on a system of engagement

- Relying on Big Data: integration of customer context

What is the significance of this for banks and bank customers?

It comes down to this:

Where multichannel has a bank-centric viewpoint, a modern omnichannel banking solution is entirely customer-centric.

In summary, this means:

- The full integration of the channels that customers use habitually, making the bank accessible without any special effort. Also, customers can be transitioned to more secure channels when needed, without interruption.

- The full history and customer information profile is always present, regardless of channel jumps and conversation switches.

- Using channels in combination to maximise the benefits of their specific capabilities.

- Human contact and the services delivered in an automated manner work together harmoniously, and customers are never left hanging, wondering how to progress their query.

- The coherent nature of interaction data allows the bank to proactively introduce services and products when they might be most beneficial and welcome, as part of the tailored support for each customer.

- The customer can pick up the channels of their choice and move between them to progress their case.

What to look for in an omnichannel technology provider

With this new understanding, what should you look for in a provider of omnichannel platforms?

- There is no such thing as a one-size-fits-all omnichannel banking solution. Each situation is different and requires customisation. Make sure your provider has the ability to listen carefully and work closely with you to define a tailored solution.

- Don’t underestimate what’s at stake when making a decision that can have a significant impact on customer experience. The quality of the relationship between your bank and its customers is on the line! Make sure the solution provider is properly able to understand your customers’ needs.

- Find a provider that understands the importance of UX and can put that understanding to work for your customers, across all touch-points, from the briefest interaction (email) through to the fullest (video-calls with screen sharing). Make sure the solution provider has user experience specialists on their team.

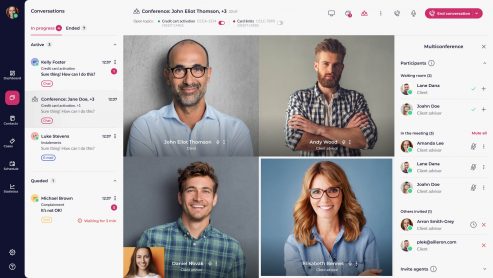

We at LiveBank are happy to say we are an omnichannel solutions provider that displays all these qualities. If you wish to find out more about this vision for omnichannel banking or discuss your needs with an expert provider in this field, please feel free to contact us!

Conclusion

By now, you probably have realised that this vision of a customer-centric banking experience has the power to deliver on the original omnichannel promise finally. It can ignite a customer-relations revolution for online banks and traditional banks too. That outcome becomes much more attainable when the omnichannel solution is in harmony with your customers’ existing habits and their banking needs. To make sure this happens, we recommend you collaborate with a specialist provider with a platform approach, one who is ready to carefully tailor the platform to fit the environment you and your customers operate within.

If this article was of interest to you and you wish to hear more about this subject in the future, you can also follow us on Linkedin.