As innovations in technology spread throughout the world, banks embarked on paths of rapid change which have gathered pace and will continue into 2020 and beyond. Disruptive technologies, including AI, machine learning, and robotics process automation are going to determine future successes and provide a wide range of opportunities.

A couple of years ago, banks and financial institutions were presented a challenge, namely, embrace the changing world of finance or fall by the wayside. Now is the time to reap as many possible benefits from technological improvements in the financial landscape as possible. To not fall behind the market, banks need to make a choice: shape the future, follow trends or put off changes. Standing still is not an option, as inaction will simply open the door to new, disruptive operators, who offer innovative, cutting-edge products and new channels to reach customers. Their processes, technology and organizational culture represent a forward-thinking strategy created to build advantages and defeat weaker competitors.

Here we present the pivotal digital trends in banking worth following in the near future. Digitization is an ongoing process, developing exponentially over the last several years which will keep enhancing and transforming the banking industry.

Table of Contents

Customer experience, the most important factor

38% of banking industry customers pointed to user experience as the most important criterion for choosing a digital bank (Source: Digital onboarding for financial services).

The fact that today’s customers need independence and swift access to banking products isn’t surprising. People have become much more international and mobile, so flexible, seamless interactions with their service providers is a natural requirement. As clients started comparing financial services to the services provided by other businesses, such as Netflix or Spotify, expectations changed. People are more likely to use platforms where personalization plays a pivotal role and where they’ll find offers tailored to their own preferences. By using these services, customers demonstrate their needs and reveal their satisfaction, which act as vital sources of data and information. The important thing is to think them through carefully, manage them properly, ensure security of their processing and present dedicated solutions. Certainly, an individual approach requires greater involvement but will pay off by increased interest and positive brand perception. Ignoring signs from consumers is fatal and without satisfying solutions customers, even loyal ones, will switch banks.

Digital evolution – branch banking transformation

As technology moved banking online, reduced cash payment usage and enabled remote access to services, a popular conclusion was that physical branches were no longer needed, though this is not entirely true. Their activity will still be important but the scope will change. First of all, real contact between clients and the bank advisors they interact with will always be required and available. The change will occur in communication tools – from traditional methods to digital channels.

Banks should use different service models geared to various end-user groups:

- Digital only customers who most likely want to accomplish every operation through internet or mobile banking

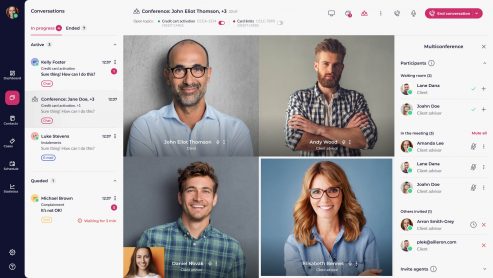

- Digital only customers who still need personal support through communication channels like chat, audio, video, email, social media messaging tools. Digital customer journeys should be enhanced by these touch points to provide product and service support through smart conversational banking platform, like LiveBank

- Customers who use traditional channels like contact centers. Voice channel still represents a major remote communication channel, however there is a shift from contact centers to conversational banking platforms because of the competitive advantages of text-chat communication over voice.

- Customers who use physical branches. Banks are educating customers about fast and convenient digital processes, and one of the solutions is deploying a VTM channel together with video, audio and chat channels in order to ensure swift access to remote advisory assistance, along with minimizing potential queues in bank branches.

Due to the higher operational costs brick and mortar bank branches generate, they will be reorganized and take new forms such as financial consulting centers or spots, where people can deal with specialists. Many leading banks have already started reducing the number of bank branches and staff employed there. In countries where the market is sated with bank branches, it is expected that a 20% decrease in their number will occur by 2020 (Source: Retail Banking 2020: Evolution or Revolution?).

When digitization became quotidian and the majority of banks had to face significant changes in order to adapt to customers’ needs and market demands, new development strategies appeared in the banking industry. Research conducted on over 400 global bank executives by The Economist Intelligence Unit (EIU) on behalf of Temenos, indicated that as many as 36% of them want to build a greenfield digital bank. Drawing on specialized knowledge in the fields of banking, compliance, and security, banks want to create a new, digital-first brand, completely removed from old methods and systems. Anticipating this growing trend, many banks have already decided to build a profitable digital bank and so Ailleron offers Bank in the Box, a state-of-the-art, modular and open digital banking platform. Greenfield digital banking demands building everything from scratch but also means avoiding restructuring obstacles, as new brands will already be born digital.

The wave of AI deployments

Year by year the importance of technology will be greater, and deploying AI solutions in banking will testify to effective tactical operations. Since services will be far more personalized, AI techniques are needed to analyze behavior, information and discover customers’ demands and to eventually build an intelligent conversational banking platform. Although thus far the banking industry hasn’t implemented AI solutions on a broad scale, in the next few years we will witness their full integration into day-to-day business. In 2019 the digital banking mainstream was led by chatbots, which were incorporated into many banks’ strategies to help solve basic problems and create a more customer-connected bank. It is predicted that by 2022 chatbots will be responsible for costs savings of over $8 billion annually (Source: Juniper Research). AI-driven solutions not only cut operating costs, they provide instantaneous, round-the-clock assistance, which is urgently required today. Furthermore, they automate work process and provide an invaluable source of the feedback and data necessary to create customized products and services.

Smart banking will be a motto of the future financial world. It will demonstrate a bank’s attitude to customers’ needs and its willingness to make changes. Managers should be aware of the fact that nowadays a cognitive attitude to customer expectations is connected with embracing AI tools for banks.

Top challenge: cyber security

Unfortunately, cyber threats have grown along with increasing online activity. These risks go hand in hand with the tremendous speed of technological development, global data exchange and open banking, which enables third-parties to access customers’ data.

The newest source of risk that is becoming more prevalent is IoT. As a fascinating solution, which significantly eases everyday activities, it also tests a bank’s security system and threatens clients’ data security. How? Banks establish cooperation with producers of mobile devices, such as smartwatches or fitness trackers, enabling mobile payments. If banks do not have appropriate protection, companies dealing with the service of these devices may not keep up with patching all security holes. As a result, hackers have much easier access to personal data. The more devices attached to the process, the higher the risk of being hacked.

Establishing a functional and consistent risk management plan that responds to evolving regulations (especially AML and CTF), while at the same time not raising costs and diminishing the customer experience, will be key in the immediate future. Cyber security is now a top challenge due to new technologies that expose clients’ data to greater dangers, but also an opportunity to out-class the competition.

Trust in blockchain

In an era of high-risk cyber-attacks and tightening regulatory requirements, a fraud-resistant system used to protect and authenticate transactions can revolutionize the financial services sector. How? Blockchain is a decentralized database, therefore it is less prone to cyber-attacks than traditional bank ledgers. Irreversibility and the inability to make changes are factors that increase safety, and a permanent historical record is a backup of all operations that ensures their authenticity. In the traditional model, all information is located in one place, secured with obsolete security systems, easy to be bypassed by hackers.

Furthermore, the blockchain system decreases operational costs and administrative burdens, since it can be implemented in diverse areas such as payments, contracts, applications, insurance or trade financing, while improving the time-consuming EKYC process. One disclosure of KYC documents can be used by other banks and authorized organizations, so once a customer’s ID is checked and verified, there will be no need to repeat the KYC process. In line with customers’ expectations, a great advantage is the introduction of real-time payments.

Clearly, leveraging blockchain in the financial industry can contribute to maximizing effectiveness, which is the strategic goal of every bank. However, if the perception and trust in such systems do not change, the presented business benefits won’t materialize.

Digital banking future trends – summary

Seemingly, the immediate future of the banking industry is quite clear. Although it’s impossible to predict the future of the financial world precisely, we do know that technological innovations will shape banks’ activity. Developing a winning strategy is founded on an open attitude to upcoming changes, evolving regulations, and customer demands. A bank’s mission should be to adopt an appropriate approach towards this rapidly changing reality.

Livebank is a conversational banking platform which enables banks to build an effective communication hub.

Ailleron’s fintech actively shapes the world of digital banking and we know that in the next few years embracing new technologies will be crucial for those organizations that want to maintain a high market position. Both banking and technology are changing rapidly, which is why we take into account prevailing and predictable trends in product development. In this way, we can provide our clients with tools that meet their needs, guarantee high-security standards and deliver the latest and most desirable technological solutions simultaneously.

By introducing technology based on artificial intelligence into our products, we created a chatbot that combines machine working capabilities with a human touch and is a tool that greatly improves customer service. To assist bank employees and customers, Ailleron also created the AI Prompter, a function of an agent’s application which fulfills the role of an ideal co-worker, not only aiding in customer service, but providing on the spot training for employees. With its ability to recognize words and analyze language, it understands customers’ intents and provides accurate responses. Such solutions make communication effortless, much more accessible and rewarding. Most importantly for us it further demonstrates Ailleron’s leading role in shaping an agile, intelligent banking culture.