Table of Contents

Do changes in customer preference affect sales processes?

Yes. It depends on the readiness of customers to purchase a specific product remotely. In the case of complex products, even very digital customers expect assistance or a personal meeting. It is an element that banks should not overlook. A digital transformation strategy must include providing sales teams with the right tools. Within the purchasing process, customers often expect an explanation of terminology or a support agent to confirm that the way they filled out forms was correct. For example, communicating with an agent via chat is enough with simple loan forms. But in remote sales processes, banks should also consider more advanced tools such as videoconferencing, document exchange, or screen sharing.

Satisfying customers within digital channels is a real opportunity for banks

Banks now have a unique opportunity to influence customer preferences in their sales paths. The dynamics of using digital channels is an opportunity not only in terms of self-service development but also in terms of improving the quality of service. Consumers have become accustomed to checking the account balance, paying bills, or making transfers, including more and more popular instantly processed transfers to telephone numbers. The activities of digital banks in the area of accounts, cards, and loans are a challenge for traditional banks. As a result, competition is increasing in these simple product segments. Here, the advantage relates to the speed of access to the offer and the simplicity of inference.

How can impressions made during the sales process affect customer loyalty?

The first element is building a personal experience that will mitigate the risks and challenges. It requires rebuilding the customer journey, regardless of the contact channel, be it a branch, digital, or other forms of contact with the bank. Building trust in a digital context is generally a more difficult challenge. Bank branches, which may not be as convenient as digital channels, can provide warmth and empathy in dialogue, often with the same counsellor supporting multiple requests. Use the experience of your department staff to build a digital experience.

How do we increase conversion by changing the customer journey?

Let’s look at a scenario where a consumer wants to buy a property and needs funding to finance it. Their journey may look like this:

Step 1 – Search for information on the bank’s website.

Step 2 – Ask the staff on the helpline or by e-mail.

Step 3 – Meets with an in-branch adviser.

Along the way, however, the consumer has to repeat their questions or understanding (it is good if the information is consistent across different channels, it will be worse if they are not). Then they provide documents and, from time to time, call to get the status of their case. Consequently, the customer loses time and concentration on buying real estate and frustration and stress increase. Moreover, the transition from one communication channel to another is not smooth.

Now let’s look at a scenario more oriented toward the customer’s experience.

Step 1 – The customer looks for information on the bank’s website. At this point, they have the option of making an appointment.

Step 2 – The customer decides to make an appointment. They can choose to authenticate themself as a bank client or remain anonymous.

Step 3 – After logging in to Internet Banking, the customer can arrange a call with an advisor of their choosing.

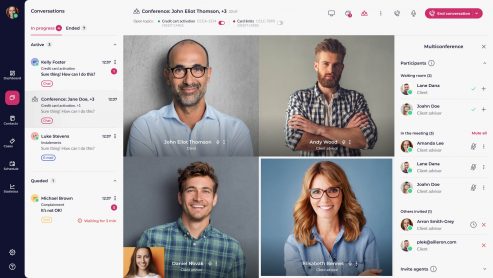

Step 4 – The advisor is assigned to the customer, and they can contact each other via chat or video.

Here, customers have access to the entire process path. Customers can see how far progressed their case is and what actions are next. They can contact the assigned advisor and, if absent, leave a message. The customer does not have to share anything a second time – the journey is consistent, regardless of which channel they choose. The physical and digital channels begin to merge, and customers are free to migrate between them.

Effect

Our internal statistics show that banks that consider the aspect of communication with an advisor in their sales processes have up to twice as high conversion rates compared to the same process without assistance. The change is a permanent change seen in the statistics over months and years. It shows the combined effect of many channels and the experience of being in contact with a living person. It is a qualitative leap or, in fact, the next stage in the evolution of the approach to digital channels.

Conclusion

Consumers are now much more aware of the functions of digital banking. Many users are comfortable with transactional banking. Remote sales are the driving force behind banks, which aligns with customers’ expectations of being able to buy financial products digitally. Digitisation should go hand in hand with the option to communicate with a living person, especially for complex interactions where conversations and advice are integral to making important decisions and overcoming stressful moments in consumers’ financial journeys. Those banks that “humanise” and create consistent sales processes achieve higher conversion rates and change purchasing preferences.